Malaysia Satellite Internet 2026: Three Orbits, Two Powers, and the APAC LEO Laboratory

Malaysia is Southeast Asia's clearest multi-orbit satellite market: Starlink operates today, MEASAT anchors the national GEO layer, and SpaceSail remains a strategic option whose commercial arrival is not yet proven.

Author

Dylan

Singapore Space Agency

Published

24 Jun 2026

Last updated

24 Jun 2026

50 min read · 8,895 words · Market Intelligence

Quick summary

What this article answers

- Malaysia is not yet a three-way commercial contest: Starlink and MEASAT operate today, while SpaceSail remains an unlicensed strategic option held through a non-binding MoU.

- East Malaysia is the binding geography; Sabah and Sarawak hold 60% of the land but 17% of the population, making satellite a primary broadband option where fibre economics fail.

- The likely outcome is segmentation—Starlink in enterprise and maritime, MEASAT GEO in broadcast and government, and a possible later MEASAT–SpaceSail offer for public programmes.

- The decisive political-economic test is the 2033 Starlink licence renewal, when enterprise stickiness and the credibility of a national alternative will re-price the foreign-ownership exemption.

This is the third article in the "APAC From the Ground Up: A Market-by-Market Guide to LEO Connectivity" series (MGT-03), focused on Malaysia — Southeast Asia's clearest multi-architecture satellite market, where an operating American LEO service, a national GEO incumbent, and a future Chinese LEO option are being assembled inside one policy and commercial landscape. The series has previously covered Indonesia (MGT-01) and Australia (MGT-02); the Philippines, Vietnam, India and a regional synthesis follow.

Executive Summary

Malaysia is Southeast Asia's clearest multi-architecture satellite market — but the three layers are not equal, and saying so is the first act of honesty this analysis requires. Starlink is an operating, fully licensed LEO service. MEASAT anchors the national GEO layer across broadcast, government and enterprise. China's SpaceSail (Qianfan) has secured a strategic route to market through a non-binding MoU with MEASAT — but it is not yet licensed or operational in Malaysia. So this is not yet a three-way commercial contest; it is two satellite layers running today while a third is held as an option. The reflex is to call the result fragmentation. It is the opposite: the policy outcome is diversification — by a government that learned, across fifty years of satellite policy, that digital sovereignty is less about owning the spacecraft than about ensuring no single vendor, and no single great power, can hold national connectivity hostage. Whether every individual decision was designed as a US–China hedge is not publicly documented (see §8); the effect plainly is.

On paper, Malaysia barely needs satellite. Its national digital infrastructure is the most prepared in ASEAN: JENDELA Phase 1 reached 99.71% populated-area internet coverage by end-2025,^[1] and the country has built two competing 5G networks.^[2] Satellite should be a marginal complement.

But paper is not terrain. East Malaysia — Sabah and Sarawak, on Borneo — is 60% of the national land area and 17% of the population, and its interior is rainforest, river, mountain and island where fiber economics simply do not close. 5G in Sarawak sits near 63.8% of populated areas and Sabah 68.6%, against a peninsular norm well above 90%.^[3] The flagship RM2 billion SALAM submarine cable announced in Budget 2026 will eventually connect Johor to six landing points across Borneo — but it solves backhaul, not last mile, and it has not broken ground.^[4] For the interior, satellite is not a complement. It is the only plausible route to broadband parity with the peninsula.

The honest picture is one of three structural tensions:

First, the three-orbit game. In February 2025 MEASAT — Malaysia's de facto national satellite operator — signed an MoU with China's SpaceSail (Qianfan) covering LEO broadband, direct-to-device, IoT and Earth observation, plus a joint Q/V-band rain-fade study.^[5]^[6] MEASAT's own GEO fleet still serves government, broadcast and enterprise. And Starlink, licensed in July 2023 with a rare 100%-foreign-ownership exemption, sells direct to consumers and bypasses MEASAT entirely.^[7]^[8] No other ASEAN market assembles all three under one roof — even if, today, only two of them actually carry traffic.

Second, the sovereignty calculus. Anwar Ibrahim's government waived Malaysia's 49% foreign-equity cap for Starlink on "national benefit" grounds^[8] — while deepening Chinese digital infrastructure: ZTE rebuilding Sarawak's state backbone,^[9] Huawei and ZTE splitting the second 5G network,^[10] and the SpaceSail–MEASAT orbit deal. This is not incoherence. It is portfolio diversification: Starlink for what it delivers today (enterprise, maritime), Chinese technology for what it delivers at scale (5G, fiber, future LEO), MEASAT for what must stay national (broadcast, government backhaul, spectrum).

Third, the East Malaysia equity gap. Peninsular Malaysia is a mature mobile oligopoly — CelcomDigi (~41% share, 20.2 million subscribers), Maxis (~26%), U Mobile (~20%) — competing on 5G speed and price.^[11] East Malaysia is a geography problem the market cannot solve unaided, which is why JENDELA 2's RM-funded, regulator-run rollout of 2,700 sites for ~217,000 residents explicitly names satellite as a delivery technology.^[12] The question is not whether satellite serves East Malaysia. It is which constellation, on what commercial terms, with what geopolitical alignment.

The call. Malaysia is neither a "Starlink market" nor a "Qianfan market." It is a multi-orbit testbed, and the winner will not be decided by megabits. It will be decided by the alignment of three things: commercial fit with Malaysian enterprise demand; the regulator's tolerance for foreign ownership and data routing; and the durability of the Malaysia–US–China triangle. The most probable outcome is not monopoly but segmentation — Starlink in enterprise/maritime/aviation, MEASAT GEO in broadcast and established government services, and a possible MEASAT-Qianfan offer in later rural and public-sector programs if Qianfan becomes operational, reliable and licensed in Malaysia. So the decisive uncertainty is not which constellation advertises the highest speed; it is whether SpaceSail can convert a strategic MoU into a functioning, licensed service before Starlink becomes too embedded in Malaysia's enterprise and public-connectivity architecture to dislodge. Our judgment: the equilibrium holds through 2028, and its most likely inflection is not a technology failure but the 2033 license-renewal decision — the point of maximum political leverage over the foreign-ownership exemption.

1. Analytical Framework

This article uses four concurrent perspectives throughout — not as separate sections, but as overlapping lenses applied to the same data:

- [Researcher] Data-driven, sourced to primary documents: MCMC filings, Ookla data, Budget 2026 allocations, MEASAT and operator disclosures, ITU records.

- [Banker] Capital structure, return on capital, pricing, and the time window of structural advantage.

- [Country Head] You are in a Kuala Lumpur office facing MCMC, MNO counterparts, and a quarterly earnings call. What does the ground actually look like?

- [Geopolitics] The decade-long chess game above commercial logic — where the SpaceSail MoU and the Starlink exemption are moves, not just deals.

These four voices are in the room simultaneously. The previous articles applied the same frame to Indonesia, where the binding constraint was regulatory complexity, and Australia, where it was market clarity. Malaysia needs a different emphasis: here the binding constraint is the multi-actor competitive equilibrium and its geopolitical underpinnings.

2. Country Context: The Most Politically Engineered LEO Market in ASEAN

2.1 Geography: The Peninsula–Borneo Divide and Capital-Structure Arbitrage

Malaysia is two countries on one flag. Peninsular Malaysia (~131,000 km²) holds roughly 26 million people — about 80% of the population — and every center of finance, industry and politics: Kuala Lumpur, Penang, Johor Bahru, Putrajaya. East Malaysia — Sarawak (124,450 km², 2.6 million, 21 people/km²) and Sabah (73,600 km², ~3.8 million) — is 60% of the land and 17% of the people, resource-rich and infrastructure-poor.

[Researcher] The peninsula–Borneo digital divide is not policy neglect; it is physics and economics. Sarawak is larger than England, blanketed in rainforest and cut by major rivers (the Rajang runs 563 km), so its communities are reachable mainly by boat. Sabah is split by the Crocker Range and Mount Kinabalu (4,095 m), with an eastern arc of remote towns and islands. Trenching fiber across this terrain runs several times the peninsular cost, and at 21–52 people/km² the payback never arrives within a rational discount rate.

[Banker] This is where LEO's advantage is misread as "speed." It is capital-structure arbitrage. A Starlink terminal is a one-time hardware cost plus a fixed monthly fee, active in minutes, with a predictable opex line. The equivalent fiber drop to an interior longhouse demands hundreds of thousands of ringgit in trenching and backhaul — if the terrain permits it at all. Two technologies, two entirely different marginal-cost curves. LEO does not win East Malaysia by being faster than fiber; it wins by making the cost of distance disappear. The same logic the Indonesia analysis drew across 17,000 islands holds here across one large, roadless island.

Table 1 — Malaysia geographic and digital-infrastructure asymmetry (2025)

| Metric | Peninsular | Sabah | Sarawak |

|---|---|---|---|

| Land area (km²) | ~131,000 | 73,600 | 124,450 |

| Population (m) | ~26.0 | ~3.8 | 2.6 |

| Density (per km²) | ~198 | ~52 | 21 |

| 5G coverage, populated areas | >90% | 68.6% | 63.8% |

| JENDELA 2 Group-1 site share | 31.1% | 35.2% | 33.7% |

Sources: DNB/MCMC coverage disclosures;^[3] JENDELA 2 Group-1 allocation.^[12] Densities derived from state land area and population.

The asymmetry is the whole story. The peninsula is a mature market where LEO is a niche for maritime, aviation and remote enterprise. East Malaysia is a frontier where LEO is a plausible primary broadband solution for hundreds of thousands of premises — which is exactly why 69% of JENDELA 2's first 1,000 intervention sites sit in two states holding 17% of the population.^[12]

2.2 The Mobile-First Society and the Real TAM

Malaysia's ~34 million people are heavily connected — household internet penetration is in the high-90s and mobile connections exceed population — but the aggregate hides the distribution. Urban penetration is effectively universal; the interior of Sabah, Sarawak's ulu (upriver) communities, and peninsular Orang Asli settlements lag on both coverage and quality.

[Banker] So the satellite TAM is not 34 million people. It is the subset where terrestrial economics fail: rural East Malaysian households; offshore and maritime workers; plantation estates; oil & gas platforms; domestic aviation over Borneo; and remote public services (clinics, schools, border posts). In served-population terms that is perhaps 2–3 million people — but be careful with the unit: what actually bills is connections, not headcount. A longhouse, a school, a clinic or an estate office shares one terminal; an offshore platform takes one or two; and some of that "gap" population will be picked up by FWA, microwave or fiber, not satellite. So the addressable terminal base is far smaller and lumpier than the population implies: a high-value enterprise and maritime core of perhaps 15,000–25,000 terminals that carries most of the margin, plus a larger but lower-ARPU residential and subsidized-public tail that, in equilibrium, could grow the total billable base into the low six figures by 2030 (the §11 model builds on exactly this split). What the core lacks in volume it makes up in ARPU: low-alternative, high-willingness-to-pay demand. At ~US$13,000 GDP per capita Malaysia is upper-middle-income, and Starlink's ~RM220/month residential plan is roughly double a median fiber plan — out of reach for the rural mass market on a pure-commercial basis. Which is why the residential rural story is government-subsidized, not market-led; the commercial engine sits in enterprise (§7).

2.3 From Palapa to MEASAT: Foreign Technology, National Control

Malaysia's satellite history is shorter than Indonesia's but no less political. Before 1996 it leased foreign capacity (Indonesia's Palapa, Intelsat, AsiaSat). The MEASAT project, championed under Mahathir as a prestige initiative, put MEASAT-1 and -2 in orbit in 1996 at 91.5°E — foreign-built (Hughes), foreign-launched (Arianespace), nationally controlled. That template — foreign technology, national control — is the through-line that explains the Qianfan partnership today.

[Geopolitics] This is the cleanest contrast with Indonesia. Jakarta's Palapa-era reflex treats foreign constellations as threats to national unity, which is why it throttles Starlink with per-gateway approvals.^[20] Malaysia's MEASAT reflex treats satellite as a national asset to be leveraged — so when the national operator can bolt Chinese LEO capacity onto its portfolio, that reads as a win, not a concession.

Table 2 — Malaysian GEO satellite fleet at 91.5°E

| Satellite | Launched | Vehicle | Bands | Status |

|---|---|---|---|---|

| MEASAT-1 / -2 | 1996 | Ariane 44L | Ku | Retired |

| MEASAT-3 | 2006 | Zenit-3SL | C/Ku | Retired |

| MEASAT-3a | 2009 | Proton-M | C/Ku | Operational |

| MEASAT-3b | 2014 | Ariane 5 | C/Ku | Operational |

| MEASAT-3d | 2022 | Ariane 5 | C/Ku/Ka/Q-V | Operational |

Sources: MEASAT fleet disclosures.^[13]

MEASAT-3d, handed over by Airbus in 2022 and co-located with 3a and 3b, is the fleet's center of gravity: a 30 Gbps Ka-band HTS payload used exclusively for Malaysia, plus a Q/V-band payload built to test next-generation transmission in high-rainfall conditions.^[13] Note that last detail. The single most concrete deliverable in the SpaceSail MoU is a joint Q/V-band rain-fade study^[5] — meaning MEASAT is not pivoting from GEO to LEO. It is using its newest GEO asset to de-risk a multi-orbit future in which LEO and GEO share the same hard tropical-attenuation problem. (We found no public evidence of a "MEASAT-3e," and exclude it.)

3. Starlink in Malaysia: Strong Performance, Conspicuously Unmeasured

3.1 The Country Median Nobody Has Cleanly Published

Here is the most-quoted number in the Malaysian LEO conversation — and the most slippery. There is no published Ookla country median for Starlink Malaysia. Starlink's own Malaysian page advertises 132–248 Mbps; field deployments report lower, load- and location-dependent figures — the Kampung Kerling proof-of-concept measured 45–56 Mbps as a school backhaul.^[16] Ookla's global Starlink median sat around 100+ Mbps in 2025.^[14] Any single "Malaysia = X Mbps" figure you see, including in earlier drafts of this very analysis, is modeled, not measured.

[Researcher] That gap is itself the finding. Malaysia almost certainly performs well above Indonesia's verified and declining 40.69 Mbps^[14]^[20] — its subscriber base is far smaller, its gateways less oversubscribed, and its regulator has not throttled gateway expansion the way Komdigi has. But the direction is what matters, and Indonesia is the cautionary tale: speed degrades quarter-on-quarter once subscriber growth outruns gateway approvals. Malaysia's advantage is that it has watched that movie. Its risk is that the same plot runs if MCMC treats gateway approvals as routine licensing rather than infrastructure priority. The single number the market most needs — a clean Malaysian Starlink median — is the number nobody has produced. Treat anyone who quotes it precisely with suspicion.

3.2 Pricing and the Enterprise Premium

Table 3 — Starlink Malaysia indicative pricing (2026)

| Tier | Service / month | Hardware | Use case |

|---|---|---|---|

| Residential (Standard) | ~RM220 | ~RM1,150–3,500 | Fixed home/SME; FUP applies |

| Business Priority | ~RM550–1,100 | ~RM4,500+ | Enterprise, SLA options |

| Maritime / Mobility | ~RM2,500–5,000 | ~RM11,600+ | Vessels, offshore platforms |

Sources: Starlink Malaysia and reseller pricing; ranges vary by importer/distributor. Indicative, not official.

[Banker] RM220/month is roughly double a median fiber plan. For a KL household with fiber, Starlink is a backup or a toy. For a Sarawak longhouse with no fiber and congested 4G, it is the only option and the price is justified by the absence of alternatives. The mass-market rural affordability threshold (~RM100–150) is one Starlink does not meet — so the residential base is constrained to middle-income rural households, government-subsidized deployments, and early adopters. The money is elsewhere: a single maritime/offshore contract can out-earn the entire residential book.

3.3 User Composition — An Estimate, Labeled as One

SpaceX discloses no country-level subscriber or revenue data, and Malaysian comparables don't transfer cleanly from Australia or Indonesia (different offshore weighting, income distribution and government-procurement structure). So rather than invent percentage shares, the table classifies each segment by evidence strength, revenue potential and confidence — which is all the public record honestly supports.

| Segment | Current evidence | Revenue potential | Confidence |

|---|---|---|---|

| Residential (rural primary / urban backup) | Available; priced at a premium to fiber | Moderate | Medium |

| Enterprise (oil & gas, plantations, mining) | Reseller focus (IEC) + clear sector demand | High | Medium-high |

| Maritime / offshore | Strong structural fit; global-plan pricing | High per terminal | High |

| Government (schools, clinics, rural) | Pilots (Kerling, UiTM) + eligible funded programs | Strategic, low-margin | Medium |

| Aviation | Long sales cycle; business-jet entry point | Long-term | Low-medium |

Strategic classification, not a subscriber count. SpaceX discloses no country-level data; shares and absolute counts cannot be sourced and are deliberately omitted. Evidence / potential / confidence are the author's assessment.

[Country Head] The government segment matters out of proportion to its revenue. The 2023 UiTM pilot (10 kits, controversially placed on already-fibered campuses)^[22] and the 2024 Kampung Kerling Orang Asli POC^[16] were signals, not businesses. The real pipeline is the funded one: Budget 2026's RM650 million for health-facility connectivity, the NADI community-center program, and JENDELA 2 (§6.3) — all of which name satellite as eligible. IEC Telecom's March 2026 Malaysia launch as an authorized Starlink reseller targeting energy, maritime, government and logistics is the market's response: a local, MCMC-licensed managed-service wrapper around Starlink's space segment.^[18]

4. The Three-Orbit Game: Two Operating Layers and One Strategic Option

4.1 MEASAT: A Capital-Constrained Incumbent Becomes a LEO Wholesaler

[Researcher] MEASAT is Malaysia's de facto national satellite operator, but — contrary to common assumption — it is privately controlled (through Ananda Krishnan's Usaha Tegas), not a Khazanah subsidiary, and it has been balance-sheet-constrained: loan covenants restricting fresh capital drove a 2021–22 privatization-and-restructuring.^[17] That financial reality is the key to reading the SpaceSail deal.

[Banker] A pure-GEO operator in a LEO world is a declining-value proposition, but MEASAT cannot self-fund a constellation — that is a US$10–20 billion bet it has no balance sheet for. The MoU resolves the bind elegantly: MEASAT contributes ground segment, customer relationships and regulatory navigation; SpaceSail contributes the space segment. MEASAT gains multi-orbit capability with no constellation capex and an asymmetric payoff — if Qianfan matures (stable service, ~2028–2029) it adds high-margin LEO wholesale to its GEO book; if Qianfan fails, MEASAT's downside is limited to business-development cost and the MoU is non-binding. For a capital-constrained incumbent, this is the rational move, not a bold one.

Table 4 — The MEASAT–SpaceSail (Qianfan) MoU, February 2025

| Element | Detail |

|---|---|

| Signed | 6 Feb 2025, Shanghai (MEASAT COO Yau Chyong Lim; SPACESAIL president Jason Zheng) |

| Scope | LEO broadband, direct-to-device, satellite IoT, Earth observation |

| Technical | Joint Q/V-band rain-fade study |

| Model | MEASAT as wholesale distributor / multi-orbit integrator |

| Status | Non-binding MoU; commercial service contingent on Qianfan maturity (3–5 yr) |

Sources: Via Satellite, SpaceNews, MEASAT.^[5]^[6]

[Geopolitics] Note what this MoU is and is not. It is a corporate agreement signed in Shanghai between executives — not, as sometimes framed, a ministerial signing ceremony staged around bilateral anniversaries. The geopolitical weight is real but inferential: it slots into the broader Malaysia–China digital relationship, and it gives Beijing a Southeast Asian beachhead through a trusted national operator. But it is an option, not a launch. Reading it as a done deal overstates Qianfan's readiness; reading it as mere PR understates what a national operator's endorsement is worth in a government-procurement market.

4.2 Qianfan's Beachhead — and the Debris-and-Latency Reality

[Researcher] Qianfan (千帆, "Thousand Sails"; operator Shanghai Spacecom / SpaceSail, backed by the Shanghai municipal government) had reached roughly 200 satellites in orbit by June 2026, against a Phase-1 target of 1,296 and an eventual ~15,000.^[7] Its international sequence — Brazil (TELEBRAS), Kazakhstan, Malaysia (MEASAT), Thailand (National Telecom) — makes Malaysia its Southeast Asian hub: MEASAT's relationships and ground infrastructure can, in principle, extend Qianfan into neighboring markets without it building distribution from scratch.

[Banker] But the readiness gap is wide, and honest. Qianfan's deployment has been troubled: its first launch in August 2024 was followed by a Long March 6A upper-stage breakup that scattered 700–900+ trackable debris fragments at ~800 km — the second such CZ-6A fragmentation, and in the same altitude band as the constellation itself.^[15] Its operational shells sit higher than Starlink's ~550 km, but — to correct a common error — that is not where any latency disadvantage comes from: a few hundred kilometres of extra altitude is only a millisecond or two of path delay, invisible in real use. The real gap is ground-segment maturity: a young constellation's true latency, throughput and reliability depend on gateway density and routing maturity, none of which Qianfan has yet demonstrated at scale or had independently benchmarked. The honest near-term read: Qianfan is better understood as an emerging capacity layer — closer in role to high-throughput GEO than to a proven low-latency Starlink substitute — than as a like-for-like competitor today. And the debris record is a launch-vehicle failure, not a MEASAT one; MEASAT cannot be blamed for it, but it is an ESG and due-diligence problem MEASAT would have to resolve before converting the MoU into a public-facing service — another reason the partnership stays an option, not a commitment.

4.3 Starlink's Paradox: Best Operations, Structural Disadvantage

[Researcher] Starlink holds the best hand on every operational metric — performance, the deepest regulatory integration (100% ownership, 10-year license, explicit government endorsement), and the most complete product line. Yet it faces a structural disadvantage in precisely the segments that anchor long-term revenue: government and rural broadband. Malaysian public procurement weights Bumiputera participation and national alignment, and the 100%-foreign exemption — granted by ministerial discretion, time-bound to 2033 — is politically exposed. The 2023 "doesn't make sense" backlash over buying Starlink kits for already-fibered campuses^[23] showed how quickly a fully American-owned vendor drawing public funds becomes an opposition talking point when a "national" alternative (MEASAT-Qianfan) is on offer.

[Banker] Starlink's rational response — visible in the IEC Telecom partnership — is to concentrate where the buyer is commercial and the decision is on merit: enterprise, maritime, aviation. That likely leaves it a profitable premium niche (50,000–100,000 high-value subscribers) rather than a mass-market champion (500,000+). The difference between those two outcomes is not technology. It is political economy.

5. Ground-Level Reality: The Kuala Lumpur Office

[Country Head — an illustrative scenario, constructed from typical Malaysian enterprise-procurement dynamics, not a reported transaction. The figures below are market assumptions, not a real quote.]

A Tuesday in March 2026. The country manager of a Sarawak palm-oil group calls: they've tested Starlink at three estates near Bintulu — ~95 Mbps, stable through the monsoon — and want 47 estates rolled out, ~RM2.8 million a year. You draft the proposal. Then you stop.

The client's real question is not performance. It is data routing and sovereignty. Estate data flows through a Starlink gateway to a global backbone that may transit Singapore or Australia. Does it ever leave Malaysia? You call your MCMC liaison. The answer is instructive: the NFP/NSP license requires compliance with the Personal Data Protection Act 2010, which protects data but does not mandate localization. Unlike Indonesia's Komdigi, MCMC is principle-based, not territorial. That is a regulatory advantage for Starlink — and a compliance gap for a Bursa-listed client with governance requirements.

So the deal is not a connectivity sale. It is a compliance-engineering exercise: route the contract through a local managed-service partner (an IEC Telecom-type wrapper) that runs a Malaysian network-operations center and a local breakout — encryption, traffic logging, routing transparency, audit rights — for a ~15% premium. But be precise about what that buys. A local breakout can direct egress, encrypt payloads and give the client an auditable trail; it cannot unilaterally guarantee that every packet and all metadata stay inside Malaysian jurisdiction, because the satellite-to-gateway path remains SpaceX-controlled. "Sovereign-data assurance" here means contractual and technical control, not absolute localization — and for most regulated clients that is enough. This is the Malaysian LEO market in one transaction: speed and latency are table stakes; the value, and the margin, live in the compliance architecture wrapped around the connection. It is why the reseller layer, not the dish, is where Malaysian LEO economics actually sit.

6. The Infrastructure Stack: What Satellite Competes With, and Where It's Mandated

6.1 DNB, the Dual Network, and the 46% Speed Decline

[Researcher] Malaysia built 5G through Digital Nasional Berhad (DNB), a state-owned single-wholesale-network vehicle, then reversed course to a dual-network model — forcing DNB to surrender half its 3.5 GHz spectrum (200→100 MHz) to a second network built by U Mobile, which went live in August 2025 and reached 82.9% populated-area coverage by April 2026.^[2]^[10] The transition came at a measurable cost: national median 5G download speed fell 46%, from 451.79 Mbps (Q4 2023) to 242.92 Mbps (Q3 2025).^[2]

[Banker] Where 5G reaches, LEO does not compete: 5G is faster (even degraded) and cheaper than Starlink. The competition is not "5G vs Starlink"; it is "5G + fiber + FWA vs Starlink in the gaps." And the gaps are durable — the 2,700 JENDELA 2 sites, the offshore platforms, the maritime fleet, the aviation sector. Even DNB's own ownership has now passed to the operators it once wholesaled to (CelcomDigi, Maxis, YTL Power and MOF Inc),^[24] confirming that the state's role is shifting from owning the network to funding the gaps — and satellite lives in the gaps.

6.2 SALAM: Sovereignty Assertion, Not Satellite Substitute

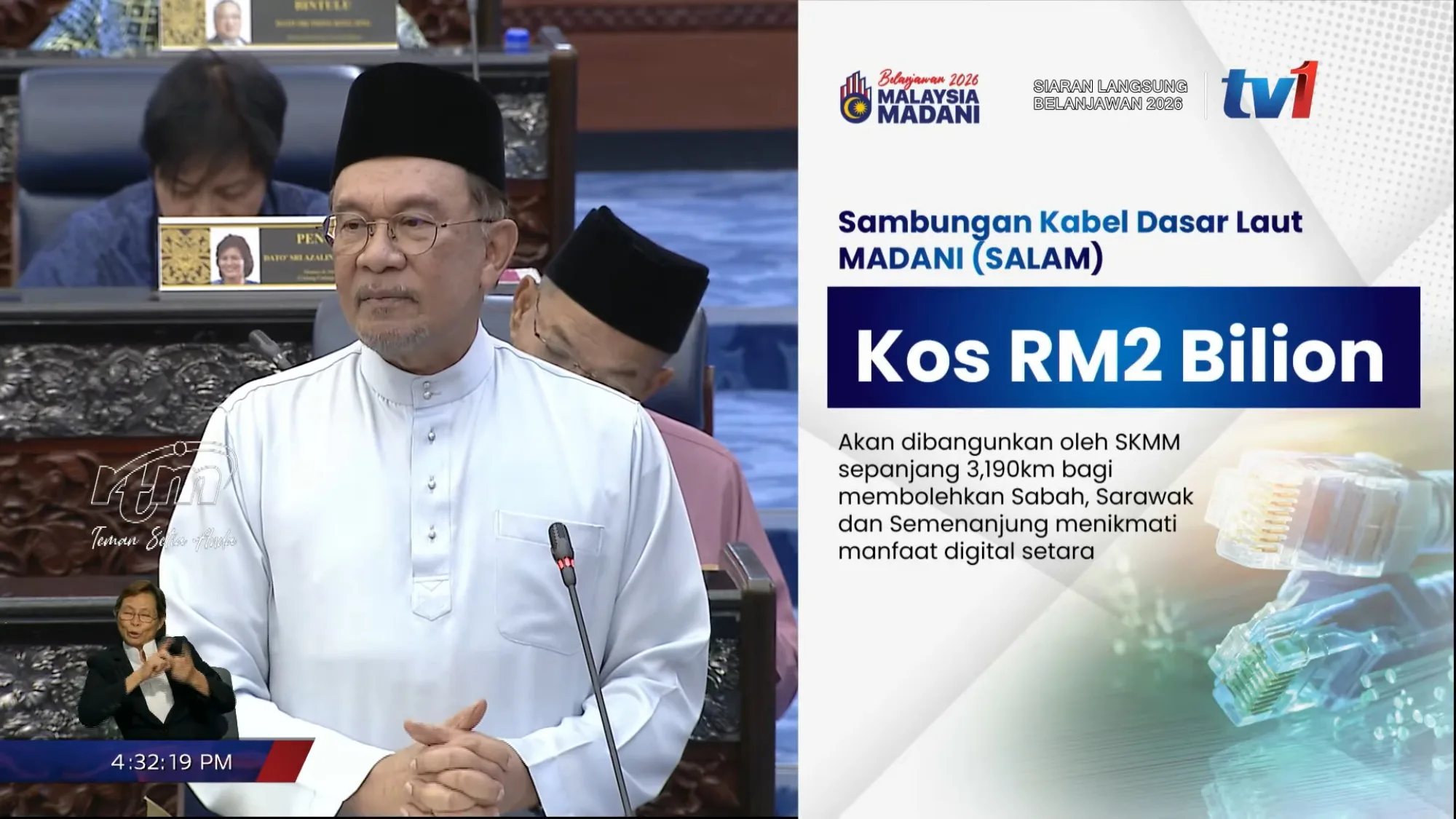

[Researcher] Budget 2026's headline digital project is SALAM (Sambungan Kabel Dasar Laut MADANI): a RM2 billion, 3,190 km MCMC submarine cable from Sedili (Johor) to Kuching and Sibu in Sarawak, then Tuaran, Kudat, Pulau Banggi, Sandakan and Tawau in Sabah — built to relieve the capacity-strained existing SKR1M/SCREAM system.^[4]

[Geopolitics] SALAM is not just telecom; it is a sovereignty assertion. East Malaysia's digital dependence on the peninsula has been a political grievance since 1963, and a direct Borneo-to-global cable (landing at Johor, hence Singapore and the subsea network) reduces that dependence. [Banker] But it does not touch satellite's core market. SALAM connects coastal cities; it does not reach inland longhouses or offshore platforms. And the timeline is the point: announced October 2025, not yet under construction, with cables of this scale typically 3–5 years to service — and a route that threads contested South China Sea waters off Sabah and Sarawak (overlapping China's nine-dash-line claims), which may further complicate permitting and laying (author inference; not an officially stated cause of delay). The 2026–2029 window — before SALAM lands — is precisely when satellite is the only high-capacity option for East Malaysia's remote interior. SALAM is a complement to satellite, not a substitute, and its lag is satellite's opportunity.

6.3 JENDELA 2: The Explicit Satellite Mandate

[Researcher] JENDELA Phase 1 (2020–2022) drove populated-area internet coverage to 99.71% by end-2025.^[1] Phase 2 targets 2,700 new sites benefiting ~217,000 residents, with Group 1's first 1,000 sites split 31.1% peninsular / 33.7% Sarawak / 35.2% Sabah — and adopts a "fit-for-purpose technology" approach that explicitly includes Wi-Fi via satellite, alongside the program's first Neutral Host Platform.^[12] MCMC issued its first call for industry plans in April 2026.

[Country Head] This is the closest thing to a guarantee of satellite's structural role. JENDELA 2 is not speculative demand; it is funded, regulator-run, publicly accountable demand in which satellite is a validated technology — guaranteed, government-backed need in thousands of locations. But timing constrains the near term, and this is where the "national champion" narrative outruns deliverability. The first awards land in 2026; a Qianfan-via-MEASAT LEO service is not deliverable before ~2028–29. So near-term JENDELA 2 awards realistically split between Starlink, MEASAT's existing GEO/HTS capacity, and terrestrial/neutral-host solutions — not Chinese LEO. MEASAT-Qianfan becomes a contender only in later phases, and only if Qianfan matures and is licensed in Malaysia. The procurement pull toward a "national" option is real; the deliverable behind the Chinese-LEO version of it is not yet there.

7. Where the Revenue Is: Enterprise Verticals

The residential rural story is subsidized; the commercial story is enterprise. Four verticals, plus a hidden one.

[Researcher] Oil & gas. PETRONAS operates 429 offshore platforms (with 10,000 km of pipelines and 34 terminals) across the South China Sea and off Sabah/Sarawak.^[19] Legacy GEO VSAT delivers 2–10 Mbps at 600–700 ms for RM50,000–200,000 per platform-year; Starlink maritime offers an order-of-magnitude more throughput at far lower latency and ~30–50% lower cost. [Country Head] But the sale is never direct: PETRONAS demands local content, offshore-certified installation (BOSIET/HUET), and data sovereignty, so the path runs through a system integrator (Sapura, Boustead-type) taking 20–30%. This is a B2B2B market, and a single large offshore account can exceed the entire residential book.

[Banker] Palm oil & plantations. Malaysia farms ~5.9 million hectares of oil palm; the major groups (Sime Darby, FGV, KLK, IOI) run estates far from fiber. The connectivity need is modest (50–100 Mbps for a central office, IoT backhaul, worker comms) but operationally essential — and increasingly an ESG-compliance enabler: buyers (Unilever, Nestlé, L'Oréal) require traceability that needs connectivity. Satellite here is not a cost; it is access to the premium certified market.

[Researcher] Maritime. The Strait of Malacca carries tens of thousands of commercial transits a year; Malaysia's 4,600 km coastline adds ports, ferries, ~85,000 registered fishing vessels and offshore support craft. Most of this is bought as part of a global maritime plan (Starlink Maritime vs Inmarsat/KVH), so Malaysia is a slice of a global contract, not a standalone market — except the deep-sea fishing fleet, where government subsidy (via LKIM) could underwrite a national program.

[Country Head] Aviation. AirAsia's 250+ aircraft are the obvious in-flight-connectivity prize, but the procurement cycle is 3–5 years and capital-heavy; the nearer-term money is business jets and charter (including oil & gas executive transport). Aviation is a slow, high-value tail, not a 2026 revenue line.

[Banker] The hidden TAM — MNO backhaul. Malaysia has ~24,000 towers; remote East Malaysian towers run expensive microwave or fiber backhaul (RM300,000–800,000 to deploy). A LEO terminal delivering ~100 Mbps of shared backhaul costs a fraction of that. If even 10% of towers adopted LEO backhaul, that is ~2,400 terminals of recurring revenue — the same undervalued backhaul opportunity the Indonesia analysis flagged, and a natural wedge for a CelcomDigi or U Mobile rather than a head-on consumer play.

8. Political Economy: Madani, the China–US Balance, and Data Sovereignty

[Researcher] Anwar Ibrahim's "Ekonomi MADANI" frames digital infrastructure as central, and the distinctive feature is explicit non-alignment in sourcing. Budget 2026 funds SALAM (RM2bn), health connectivity (RM650m), a sovereign-AI initiative, and NADI — open to multiple vendors — while the government simultaneously deepens Chinese infrastructure: ZTE rebuilding Sarawak's SACOFA backbone with full-band OTN (1.6 Tbps) and a 6-in-1 EDN processor,^[9] and the second 5G network splitting vendors Huawei (Peninsular) / ZTE (Sabah & Sarawak) with SACOFA fiber backhaul.^[10]

[Geopolitics] This is not fence-sitting; the effect is calibrated diversification. Total dependence on US technology exposes Malaysia to export controls and political pressure; total dependence on Chinese technology exposes it to leverage and supply-chain risk. The answer is optionality: American LEO for some domains, Chinese for others, national assets (MEASAT, DNB) as the sovereign backbone. But read the Starlink exemption honestly. It was granted in July 2023 — eighteen months before the MEASAT–SpaceSail MoU — so "balancing Chinese LEO" cannot have been its original motive; the documented justifications were rural and maritime benefit, no reliance on the USP fund, the Tesla/Malaysia-Digital investment relationship, and competition. Whatever the original intent, the strategic effect is diversification: Malaysia now holds a functioning US LEO option alongside deep Chinese participation in its terrestrial networks and a future Chinese LEO channel through MEASAT. That the exemption was deliberately designed as a China counterweight is a plausible reading — but it is author inference, not documented fact, and we flag it as such.

The East Malaysian backbone choice then has a quiet competitive consequence the brochures miss — though the mechanism is commercial, not technical. With Sarawak's state backbone and the eastern 5G network both running on ZTE/Huawei, a Chinese LEO layer (Qianfan via MEASAT) is easier to bundle into that stack. Not for architectural reasons — satellite-to-ground integration uses standard IP/Ethernet interfaces, and ZTE/Huawei terrestrial kit is no more natively compatible with Qianfan than with Starlink — but for institutional ones: existing vendor relationships, procurement bundling, vendor financing, integration support and a shared security-and-trust framework. In the two states where satellite matters most, the ground layer is already tilting toward the Chinese ecosystem, and that procurement gravity, more than any speed comparison, is Starlink's deepest structural challenge in East Malaysia.

[Banker] Data sovereignty as a segmentation tool. Under PDPA 2010 the default is that data must be protected, not localized — but "no blanket mandate" is not "no rules": sector regimes (Bank Negara for finance, health-data and government-security rules) and cross-border-transfer conditions can impose stricter controls than the general principle. So clients indifferent to routing (consumers, SMEs, maritime) use Starlink directly, while government, finance, healthcare and oil & gas buy managed services with a 15–30% sovereignty premium. That segmentation is profitable for Starlink and its local partners alike. The risk is policy drift: if MCMC follows Indonesia toward localization mandates, Starlink's cost base rises. The current regime is favorable — but it is not guaranteed past the 2033 license review.

9. Regulatory Framework: The Most Permissive in ASEAN After Singapore

[Researcher] Under the Communications and Multimedia Act 1998, satellite operators need Network Facilities Provider and Network Services Provider licenses, normally capped at 49% foreign equity. Starlink received NFP(I) and NSP(I) licenses on 17 July 2023, valid ten years, and a 100% foreign-ownership exemption via ministerial discretion on MCMC's recommendation — justified in Anwar's 31 October 2023 written parliamentary reply on grounds of global organizational structure, Malaysia Digital status, and rural/maritime benefit delivered "without relying on the USP fund."^[7]^[8]

Table 5 — LEO regulatory posture, Malaysia vs peers

| Malaysia | Indonesia | Australia | |

|---|---|---|---|

| Regulator | MCMC | Komdigi | ACMA |

| Foreign-equity cap | 49% (waived to 100% for Starlink) | 49% (enforced) | None |

| Gateway approval | Streamlined | Per-gateway, slow | Automated |

| Data localization | PDPA, no mandate | Sector-specific, developing | No mandate |

| Verified Starlink median | Not published | 40.69 Mbps (declining) | 162.47 Mbps |

Sources: MCMC/Komdigi/ACMA frameworks; Ookla.^[7]^[8]^[14]^[20] Australia/Indonesia per the Australia and Indonesia analyses in this series.

[Researcher] For Starlink specifically, Malaysia is among ASEAN's most permissive markets — second only to Singapore on several practical dimensions. But note the qualifier: the 100% exemption is a case-by-case ministerial waiver, not a regime-wide rule (Vietnam's pilot is time-boxed and subscriber-capped; Indonesia enforces 49%), and Qianfan itself holds no Malaysian operating license today. The primary risk is not current policy but policy continuity. The exemption is discretionary and tied to a license that comes up for renewal in 2033 — which is less a "cliff" (telecom licenses usually renew with continuity, and an embedded enterprise user base raises the political cost of any exit) than the point of maximum leverage over the foreign-ownership terms, landing exactly as the Qianfan-MEASAT partnership matures and Amazon Leo (Kuiper) potentially enters. The window is open and timed — 2033 is when the terms get re-priced, not necessarily when they end.

What would actually tip 2033 from re-pricing to non-renewal (Scenario C)? A specific, testable condition, not a mood. It flips only if, by then, (a) MEASAT-Qianfan can demonstrably deliver an equivalent enterprise/maritime service at scale — removing the "no national substitute" defense — and (b) Starlink's embedded base is still concentrated in government and subsidized accounts rather than sticky enterprise. If by 2033 Starlink has locked in PETRONAS, the plantations and the maritime fleet, non-renewal becomes economic self-harm and the exemption renews on tougher terms; if Starlink is still mostly a government-procurement vendor, it is politically expendable. That hinge — enterprise stickiness versus a credible national substitute — decides Scenario C far more than any election rhetoric.

10. The Regional Arc: Indonesia ↔ Malaysia ↔ Australia

[Researcher] Three articles, one spectrum of LEO-market maturity:

- Indonesia — largest TAM, worst regulatory friction; 40.69 Mbps and declining is a symptom of gateway bottlenecks and sovereignty anxiety.^[20]

- Australia — clearest market on earth; 162.47 Mbps reflects dense gateways, light load, and a regulator that treats satellite as rural necessity, not threat.^[21]

- Malaysia — between the two: more open than Indonesia (100% ownership, no 3T-style restrictions), less frictionless than Australia; smaller than Indonesia but more concentrated in high-ARPU verticals; less geographically extreme than 17,000 islands but more politically divided by the peninsula–Borneo split that drives government procurement.

Table 6 — Three-market comparison

| Indonesia | Malaysia | Australia | |

|---|---|---|---|

| Population (m) | ~278 | ~34 | ~26.5 |

| GDP/capita (US$) | ~4,900 | ~13,000 | ~64,000 |

| Starlink launch | May 2024 | Jul 2023 | 2021 |

| Verified Starlink median | 40.69 | not published | 162.47 |

| Foreign-ownership cap | 49% | 49% → 100% (Starlink) | None |

| National operator | Telkomsat (GEO) | MEASAT (GEO) | NBN Co (wholesale) |

| Chinese LEO partnership | None (yet) | MEASAT-Qianfan MoU | None |

| Primary LEO risk | Regulatory stagnation | Multi-orbit competition | Market-size saturation |

Sources: this series; Ookla; national statistics.^[14]^[20]^[21]

[Geopolitics] A pattern is visible — US-aligned markets (Australia, Philippines, Singapore) tend to have the clearest LEO paths and fastest Starlink; China-leaning or non-aligned markets (Indonesia, Vietnam, Thailand) tend to be more restrictive — but resist reading regulation purely as alignment. Indonesia's friction is as much about domestic-operator protection, regulatory capacity and a fifty-year sovereignty tradition as any China tilt; Singapore's openness owes as much to state capacity and market structure as to security ties; Australia's performance owes most to geography and gateway density. State capacity, domestic-operator interests, geography and data-sovereignty doctrine matter as much as bloc alignment. Within that fuller picture, Malaysia is the swing state: open to Starlink yet deepening Chinese infrastructure. If it sustains a multi-orbit, multi-power equilibrium it becomes the ASEAN template; if a great power forces a binary choice, the region risks polarizing into US- and China-aligned satellite blocs — and Malaysia is where we would see it first.

11. Scenario Analysis, 2026–2031

Scenarios are regime variables, not gradients. Probabilities are the author's assessment. The revenue figures are bottom-up, order-of-magnitude ranges — not point forecasts — and they size the satellite-broadband market across all operators and orbits; they exclude MEASAT's legacy linear-broadcast revenue, a separate and larger pool. Table 7a shows exactly how the headline number is built, so a reader can re-price any input.

Scenario A — Multi-Orbit Equilibrium (45%). Starlink, a maturing MEASAT-Qianfan and 5G coexist by segment; Qianfan reaches commercial viability via MEASAT ~2028; later JENDELA awards split. Malaysia becomes the ASEAN multi-orbit model; the satellite-broadband market reaches ~$160–230M by 2030; no single orbit dominates; the geopolitical hedge holds. Starlink Malaysia revenue ~$70–100M by 2030, enterprise-led.

Scenario B — Starlink Entrenchment (30%). Qianfan stays troubled (debris, delays); the MoU lapses; Starlink wins the bulk of satellite awards and pushes into residential/government. Starlink becomes the de facto national LEO provider (a ~200,000-terminal base), but single-vendor dependence becomes a live sovereignty risk — the Ukraine precedent (service used as leverage) is the cautionary case. Market ~$210–300M by 2030.

Scenario C — Chinese LEO Ascendancy (25%). Qianfan matures fast (1,000+ sats by 2027), MEASAT-Qianfan launches ~2027 at 20–30% below Starlink, the government steers later JENDELA awards national, and the 2033 exemption is not renewed. MEASAT-Qianfan takes the majority of the market; Starlink retreats to premium enterprise/maritime; Malaysia's stack tilts Chinese; US friction rises. Market ~$150–220M by 2030 (lower ARPU, price competition).

Table 7a — How the market sizes: illustrative 2030 bottom-up (Scenario A, satellite-broadband)

| Segment | Terminals (2030, est.) | ARPU/month | Annual |

|---|---|---|---|

| Residential (rural-primary + urban backup) | ~110,000 | ~$50 | ~$66M |

| Enterprise (onshore O&G, plantation, mining, remote) | ~12,000 | ~$250 | ~$36M |

| Maritime & offshore (platforms, vessels, deep-sea fishing; MY-attributable) | ~5,000 | ~$750 | ~$45M |

| Government / subsidized (schools, clinics, NADI, JENDELA) | ~15,000 | ~$80 | ~$14M |

| MNO backhaul | ~2,500 | ~$600 | ~$18M |

| Aviation + misc | — | — | ~$8M |

| Total | ~145,000 | ~$187M |

The bridge the headline rests on: a high-value enterprise/maritime core of ~20,000 terminals carrying most of the margin, plus a larger, lower-ARPU residential and subsidized-public tail. Move the residential count or the maritime ARPU and the total moves with it — which is exactly why the scenarios are ranges, not points. (Maritime counts only Malaysia-attributable terminals, since vessels buy global plans.)

Table 7b — Satellite-broadband market, scenario midpoints (US$M; ±35%, illustrative)

| Year | A (45%) | B (30%) | C (25%) |

|---|---|---|---|

| 2026 | ~25 | ~30 | ~22 |

| 2028 | ~95 | ~120 | ~85 |

| 2030 | ~190 | ~250 | ~180 |

| 2031 | ~235 | ~320 | ~225 |

On these midpoints the probability-weighted 2030 figure lands around $190–210M — an order of magnitude, not a point estimate. The point is the shape: a fraction of 1% of national telecom revenue, yet high-margin, fast-growing and strategically disproportionate.

[Banker] The investment theses fall out cleanly. Starlink: not mass-market dominance but enterprise/maritime premium capture in a favorable regulatory window. MEASAT: multi-orbit optionality — a low-cost call option on LEO; if Qianfan works it becomes a regional distributor, if not its GEO/broadcast cash flow is intact and it can pivot to Kuiper or OneWeb. The most sensitive variable across all three scenarios is Qianfan's operational maturity: pull it forward to 2027 and the map tilts to C; push it past 2030 and Starlink gets a 3–4-year entrenchment runway (B).

12. APAC and Singapore Implications

[Geopolitics] Malaysia's experiment is the most detailed case study yet of how a mid-sized, non-aligned economy navigates LEO geopolitics — and three lessons travel:

- Regulatory architecture beats technology. The same constellation delivers ~40 Mbps and falling in Indonesia and almost certainly far more in Malaysia. The variable is the regulatory ground it stands on, not the hardware.

- National operators are adaptation mechanisms, not obstacles. MEASAT shows a capital-constrained GEO incumbent becoming a LEO enabler — the "national operator as wholesale LEO distributor" model is replicable across ASEAN markets that cannot fund their own constellations (Telkom, Thaicom, PLDT).

- Sovereignty in the LEO era is optionality, not ownership. Malaysia owns no constellation and never will. It owns options — American LEO, Chinese LEO, national GEO — and that portfolio is the realistic template for the region.

[Researcher] The Singapore dimension. Singapore's own satellite demand is small (urban, near-universal fiber/5G), so its interest in Malaysia is strategic, not commercial: what does a multi-orbit, multi-power market over ASEAN mean for regional cybersecurity, spectrum and debris coordination, and cross-border data flows? As the Indonesia analysis argued, Singapore's edge is as the region's neutral interface layer — the trusted ground, data and coordination hub above the orbital contest. Malaysia is the live experiment Singapore should be reading as a leading indicator.

13. What to Watch: Five Signals Over 24 Months

- Qianfan's first live service via MEASAT. A real pilot before end-2027 lifts Scenario C; continued dormancy through 2028 lifts B.

- JENDELA 2 award structure. The Group-1 split between Starlink and MEASAT-Qianfan is the cleanest read on whether MCMC treats satellite as neutral or steers it nationally.

- SALAM construction start. Ground-breaking in 2026 on schedule shortens the East Malaysia satellite window; delay (maritime transit approvals, funding) extends it.

- Starlink gateway expansion. Two-plus new gateways in 2026 (Sandakan/Sibu/Miri) hold performance; a stall replicates Indonesia's degradation curve.

- The next general election and the 2033 license-renewal decision. If foreign-technology ownership becomes a campaign wedge, the terms of the Starlink exemption's renewal — and the whole equilibrium — are in play.

14. Conclusion: Malaysia as the APAC LEO Laboratory

Malaysia is not the biggest, richest, or most remote LEO market in APAC. It is the most structurally instructive — the only one assembling three architectures, two powers and one national operator at once, two of them carrying traffic today and the third (Chinese LEO) still an option held open through MEASAT.

The verdict is sharp, not hedged. For Starlink specifically, Malaysia is among ASEAN's most permissive markets after Singapore; Starlink's operations are genuinely strong (even if, tellingly, its country performance has never been cleanly measured); the enterprise verticals — 429 offshore platforms, the plantations, the straits — are high-ARPU and defensible; and the government's funded inclusion agenda turns rural demand from a market gamble into a procurement line. But the contest will not be settled by megabits. It will be settled by the alignment of commercial fit, regulatory tolerance, and geopolitical durability — and on those axes Starlink's operational lead is partly offset by a structural disadvantage in the government and rural segments, and by an East Malaysian ground layer whose procurement gravity already pulls Chinese.

The most probable outcome is not a winner. It is segmentation: Starlink in enterprise, maritime and aviation; MEASAT GEO in broadcast and established government services; and a possible MEASAT-Qianfan offer in later rural and public-sector programs if Qianfan becomes operational, reliable and licensed. Less dramatic than a monopoly — and far more stable for Malaysian sovereignty. The real question is durability: can the compartmentalization hold for a decade without Washington or Beijing forcing a binary choice? Our call: it holds through 2028, and its most likely inflection is not a technology failure but the 2033 license-renewal decision, arriving just as Qianfan matures — the moment the foreign-ownership terms get re-priced. Watch that date. For the rest of non-aligned APAC — Indonesia as Qianfan expands, Vietnam as its pilot matures, Thailand as its options multiply — Malaysia is the template being written now. Speed and latency matter here — but they do not decide the market alone. Regulation, procurement and geopolitical durability decide who converts technical performance into durable share. That is the real contest in Malaysia: not megabits, but who gets to architect the digital future from the ground up.

All data is drawn from public sources, including Ookla, MCMC, DNB, MEASAT, SpaceNews, Via Satellite, ZTE, IEC Telecom, PETRONAS/MPM, Malaysian and international reporting, and the prior Indonesia and Australia analyses in this series. Country-level Starlink subscriber, revenue and speed figures are not officially disclosed; where used, they are clearly labeled estimates or modeled ranges. Scenario probabilities and forward-looking judgments are the author's independent views and are not investment, legal, or procurement advice.

Evidence ladder — how to read the claims here. Verified fact (regulatory, sourced): Starlink's 100% exemption and 2023 license; the MEASAT–SpaceSail MoU and its scope; Budget 2026's SALAM/JENDELA allocations; the 5G speed decline; PETRONAS platform count; MEASAT-3d payloads. Company statement: Starlink advertised speeds; vendor press releases. Modeled estimate: the Table 7 revenue ranges and segment classification. Author inference (flagged in-text): the "calibrated hedging" reading of government motive; Qianfan's "Southeast Asian beachhead"; the East-Malaysia procurement-gravity advantage; the split-award and scenario calls. Scenario assumption: all 2027–2031 forward figures. Where a load-bearing claim could not be cleanly sourced — above all a Malaysian Starlink speed median — it is labeled unmeasured rather than estimated.

Confidence: High on regulatory facts, the SpaceSail MoU, Budget 2026 allocations, and operator/network data (primary and credible-secondary sourced); Medium on market sizing and scenario forecasts (modeled). Singapore Space Agency is an independent research platform. No official affiliation. UEN 53448796C.

Report date: June 2026 · Author: Dylan | Singapore Space Agency

Sources

- 1.The Edge Malaysia / Bernama — National internet coverage reaches 99.71% of populated areas by end-2025 (from 91.8%); premises passed rose 4.96m→9.81m — Communications Minister Fahmi Fadzil, Dewan Rakyat, Feb 2026(theedgemalaysia.com)

- 2.TechWireAsia — Malaysia's 5G reality check: dual network, speed decline 451.79→242.92 Mbps (Jan 2026)(techwireasia.com)

- 3.State-level 5G coverage gaps (Sarawak ~63.8%, Sabah 68.6% of populated areas) per MCMC/JENDELA reporting and DNB coverage disclosures, 2025–26; context via The Edge Malaysia — JENDELA: internet coverage in populated areas of Sarawak and Bernama — JENDELA 2 rural-connectivity solutions. B-grade; state-level 5G percentages are secondary-reported and should be treated as indicative.

- 4.Lowyat.NET — Budget 2026: MCMC to develop MADANI (SALAM) submarine cable system — RM2bn, 3,190 km, Johor→Sabah/Sarawak (Oct 2025)(lowyat.net)

- 5.Via Satellite — MEASAT Signs MoU With China's SpaceSail LEO Constellation (6 Feb 2025)(satellitetoday.com)

- 6.SpaceNews — Chinese constellation operator Spacesail signs agreement with Measat of Malaysia (Feb 2025)(spacenews.com)

- 7.Malay Mail — MCMC: Starlink allowed to operate in Malaysia as a 100% foreign-owned entity; NFP(I)+NSP(I) licenses, 17 Jul 2023, 10-year validity (25 Jul 2023)(malaymail.com)

- 8.The Star — Tesla, Starlink allowed 100% foreign ownership due to benefits for nation, says PM Anwar (parliamentary reply, 1 Nov 2023)(thestar.com.my)

- 9.ZTE — SACOFA partners with ZTE to modernize SACOFA's statewide network in Sarawak — full-band OTN (1.6 Tbps), 6-in-1 EDN (Sep 2025)(zte.com.cn)

- 10.SoyaCincau — U Mobile signs Huawei and ZTE for Malaysia's second 5G network (Huawei: Peninsular; ZTE: Sabah & Sarawak) (15 Apr 2025)(soyacincau.com)

- 11.The Malaysian Wireless — CelcomDigi 20.2m subscribers (~41% share), Sept 2025(malaysianwireless.com)

- 12.Malay Mail — MCMC calls for submissions under JENDELA 2: 2,700 sites, ~217,000 residents; Group-1 1,000 sites split 31.1% Peninsular / 33.7% Sarawak / 35.2% Sabah; fit-for-purpose incl. satellite Wi-Fi and Neutral Host Platform (1 Apr 2026)(malaymail.com)

- 13.MEASAT — MEASAT-3d fleet page: launched 22 Jun 2022 (Ariane 5, Airbus); co-located 91.5°E with 3a/3b; 30 Gbps Ka-band HTS for Malaysia; Q/V-band high-rainfall payload(measat.com)

- 14.Ookla — Global Satellite Broadband Performance Report (2025–26)(satellitetoday.com)

- 15.SpaceNews — Chinese (Long March 6A) rocket stage breaks up into 700+ pieces of space debris at ~800 km after first Qianfan launch (Aug 2024)(spacenews.com)

- 16.The Star — Kampung Orang Asli Kerling first Starlink POC in Malaysia (Teo Nie Ching): Starlink backhaul to JENDELA tower 7.5 km away; 45–56 Mbps for 260 residents + 100 students (9 May 2024)(thestar.com.my)

- 17.The Edge Malaysia — Cover Story: MEASAT — ownership (Usaha Tegas / Ananda Krishnan) and 2021–22 privatization/restructuring under capital constraints(theedgemalaysia.com)

- 18.IEC Telecom — IEC Telecom Enters Malaysia as an Authorized Starlink Reseller (3 Mar 2026); enterprise focus: energy, maritime, government, logistics; MCMC-licensed(iec-telecom.com)

- 19.PETRONAS / Malaysia Petroleum Management — Malaysia E&P overview: 429 offshore platforms, ~10,000 km pipelines, 34 terminals(petronas.com)

- 20.Singapore Space Agency — Indonesia Satellite Internet: Starlink's 17,000-Island Opportunity and Three Structural Constraints (MGT-01)

- 21.Singapore Space Agency — Australia Satellite Internet 2026 (MGT-02)

- 22.Malay Mail — UiTM getting 10 Starlink kits though campuses already have fibre broadband (24 Jul 2023)(malaymail.com)

- 23.MalaysiaNow — "Doesn't make sense": Anwar's quick purchase of Starlink kits draws fire (25 Jul 2023)(malaysianow.com)

- 24.The Edge Malaysia — DNB stake taken over by CelcomDigi, Maxis, YTL Power and MOF Inc(theedgemalaysia.com)

Continue reading

3 May 2026 · 55 min read

Indonesia Satellite Internet: Starlink's 17,000-Island Opportunity and Three Structural Constraints

An in-depth market analysis of Indonesia's satellite internet landscape, drawing on Ookla 2025 global data, Komdigi regulatory filings, and Telkom's annual report. How Starlink navigates regulatory friction, Telkom's dual role, and the Qianfan question in Southeast Asia's most complex market.

14 May 2026 · 75 min read

Australia Satellite Internet 2026: The World's Clearest LEO Market and Three Lessons It Teaches

Australia delivers Starlink's best Asia-Pacific performance at 162 Mbps — four times Indonesia's 40 Mbps from the same constellation. This analysis dissects why: twenty ground stations, regulatory alignment, and a mature payment base. It then examines NBN Co's historic Amazon Leo deal, Telstra's Direct-to-Cell pioneering, the JP9102 defence cancellation, Starship's geographic opportunity, and what a functioning dual-LEO operator market looks like for the first time anywhere in the world.

1 Jul 2026 · 82 min read

Philippines Satellite Internet 2026: The Alliance Market

The Philippines is ASEAN's most geopolitically advantaged LEO market, but enterprise continuity and broad mid-tier demand—not mass residential adoption—make the economics work.