China's Orbital-Compute Mobilisation: Capital, Constraints, and the Layers That Can Actually Win

China is organising state capital, launch, satellites, silicon, and optical links around orbital compute before the sector has proved a commercial closed loop.

Author

Dylan

Singapore Space Agency

Published

23 Jun 2026

Last updated

23 Jun 2026

30 min read · 6,729 words · Market Intelligence

Quick summary

What this article answers

- China moved orbital compute from scattered experiments into formal industrial mobilisation before any operator proved a commercial closed loop.

- Capital is layered across state infrastructure, venture-backed components, downstream rocket plays, and support-layer IPOs; headline totals obscure that distinction.

- China has real in-orbit demonstrations, but launch cost, advanced silicon access, and paying repeatable workloads remain unresolved.

- Builders should target thermal, optical, ground, networking, buses, and TT&C—the layers that retain customers even if general orbital compute arrives late.

China is the one place outside SpaceX where launch, satellite manufacturing, domestic AI silicon, optical inter-satellite links, and state capital already sit inside a single industrial system — and in Q2 2026 it began organising that system around orbital compute before the sector has a commercial closed loop. This piece separates what is verified from the institutional picture from inference, and argues that the layers a Chinese builder can actually win are the picks-and-shovels — thermal, optical, ground, networking, buses, TT&C — not a copycat compute fleet.

Report date: June 23, 2026 Author: Dylan | Singapore Space Agency

This is the China counterpart to our SpaceX AI1 / IPO teardown (spacex-ai1-orbital-compute-ipo-2026) and our China's Orbital Compute Reality Check. It cross-references both rather than re-proving their numbers: the reality check scores China's individual companies player-by-player; the teardown prices SpaceX's AI1 narrative. Here we read the institutional mobilisation and translate it into builder-level choices.

Disclaimer: This article describes publicly visible institutional and capital activity and the author's reading of it. It scores no company and endorses none. Where a claim rests on a single Chinese-language source, or is the author's inference rather than a documented fact, it is labelled as such in the body and in the source grades. Analysis represents the author's independent views and is not investment advice.

1. At a Glance

In the second quarter of 2026, orbital compute in China crossed a line that has nothing to do with hardware. Key state and quasi-state institutions decided the sector is important enough to organise around — committees, an innovation centre, regional consortia, and a defence-industrial feasibility study — before commercial feasibility is established. That is the institutional shift, and it is the most important China fact of the quarter.

The capital following that shift is not one pool but four distinguishable layers: state-backed infrastructure bets, market-VC component plays, rocket firms reaching downstream, and support-layer IPOs. Conflating them is the most common analytical error; read separately, they say very different things about what is fundable.

Underneath the mobilisation, the in-orbit-versus-closed-loop gap is still enormous. China has genuine, world-class in-orbit demonstrations — and no operator showing a paying, repeatable commercial workload at scale. AI1, SpaceX's 70-metre compute satellite unveiled in June, does not change that on either side of the Pacific. What it changes is belief: it converts orbital compute from a contestable thesis into a board-level and ministry-level assumption, and it landed in the exact window China was already mobilising in.

The builder's takeaway is unsentimental. The state can fund deployment further and faster than the market would, but the unit economics China must eventually close are harder than SpaceX's — higher launch cost, gated access to the best silicon, policy-driven rather than return-driven capital. The layer that survives if the belief is early is the picks-and-shovels: thermal, optical, ground, networking, and the buses and TT&C that get bought no matter what. Pick those, not a copycat fleet.

2. AI1 as a Forcing Function, Not a New Chinese Fact

Set the minimum context first, because a reader may arrive here without having read the SpaceX piece. AI1 is SpaceX's orbital-compute satellite — a roughly 70-metre platform unveiled in June 2026, days before what was framed as the largest IPO in history. Our companion teardown argues that AI1's valuation prices narrative — an option on orbital compute — far above its verified capability. That is the Western half of the story.

AI1's contribution to China is not a new Chinese fact. It is a new forcing function: a trillion-dollar Western artefact that lands on a Chinese sector already mid-mobilisation and accelerates it. The mechanism is reflexive — belief reallocates resources before any hardware proves the belief. A $1.77 trillion company unveiling a 70-metre compute satellite is the most powerful possible external validation for a mobilisation that was already underway, and it arrived in the precise window when China's defence-industrial planners had opened a feasibility study and its industry committees were standing up.^[1] So the right way to read AI1 inside China is not as a competitor's spec sheet but as a probability-raising event that sharpens a domestic case the state had already started building.

3. Q2 2026: From Experiment to Industrial Plan

The most important China development of the quarter is not a satellite. It is the speed at which orbital compute was pulled into formal industrial planning. Read Q2 2026 as a deliberate act of consolidating fragmentation — a year of scattered company experiments gathered into committees, innovation centres, regional consortia, and a state feasibility study.

The anchor event is verifiable and official. On April 3, 2026, at the 2026 Space Computing Industry Conference in Beijing's Yizhuang economic-development zone, China stood up its first cross-industry coordination body for orbital compute — the Space Computing Power Professional Committee (太空算力专业委员会).^[2] The institutional lineage matters, because looser secondhand accounts get it wrong: the committee sits under the Computing Power Industry Development Phalanx (算力产业发展方阵), a platform convened by the China Academy of Information and Communications Technology (CAICT, 中国信息通信研究院), a think tank under the Ministry of Industry and Information Technology (MIIT).^[2] It is not an MIIT ministerial committee and not a creation of the computer-industry trade association; it is a CAICT-hosted industry-alignment body. Same conference, two further outputs: the Beijing Space Computing Innovation Center (北京太空算力创新中心) began formation under the Yizhuang management committee, targeting five directions — space-based AI chips, space energy and cooling, constellation/spacecraft, space-ground compute-network coordination, and applications — and the zone published a "key common-technology challenge list" for the field.^[3]

Two days later, the state's own hand became explicit. On April 5, Yu Guobin, deputy director of the commercial-space department at the State Administration of Science, Technology and Industry for National Defense (SASTIND, 国家国防科工局), disclosed that SASTIND has begun a feasibility study for a space-based intelligent computing constellation, having already convened the kick-off meeting and expert panels; MIIT, he added, will support the enabling layers — radiation-tolerant chips and inter-satellite laser communication.^[1] This is the signal that matters. When the defence-industrial planning body opens a feasibility study and frames orbital compute as necessary to "break through bottlenecks in ground computing," the sector has crossed from venture experimentation into state industrial planning. That framing — alongside CASC's earlier inclusion of gigawatt-class space digital-intelligence infrastructure in its 15th Five-Year Plan, which our reality check documented — is the strategic envelope every Chinese player now operates inside.^[4]

The regional and academic layers filled in over the following six weeks, and the pattern is consistent — convene, consolidate, standardise.

| Date | Event | What it signals |

|---|---|---|

| Apr 3, 2026 | Space Computing Power Professional Committee stood up under CAICT's Computing Power Phalanx (Beijing Yizhuang)^[2] | First cross-industry coordination body — institutional ownership of the sector |

| Apr 3–4, 2026 | Beijing Space Computing Innovation Center begins formation; five focus directions; common-technology challenge list published^[3] | Local government commits a physical innovation hub and a research agenda |

| Apr 5, 2026 | SASTIND discloses feasibility study for a space-based intelligent computing constellation; MIIT to back rad-tolerant chips and laser comms^[1] | Defence-industrial planning body crosses from experiment to state planning |

| May 15, 2026 | Yangtze River Delta Space-Based Computing Innovation Consortium announced (Pujiang Forum), led by Dongfang Tiansuan, 20+ members, seven core technologies^[5] | Regional industrial bloc forms around a shared technology roadmap |

| ~May 20, 2026 | CCF YEF2026 forum: "from proof-of-concept to scale deployment?" — BUPT, Galaxy Space, Fudan, Huawei 2012 Lab^[6] | Academic agenda converges on the same power/thermal/link/scheduling constraints |

| Jun 11, 2026 | Space Computing Constellation Industry Development Conference, Hangzhou (with China Mobile Communications Federation)^[7] | Convening cadence is now monthly rather than annual |

The honest read: institutionally, China is doing to orbital compute what it has done to EVs, solar, and LEO broadband before it — declare it a strategic industry, build the scaffolding early, and mobilise capital and supply chains ahead of demonstrated demand. The caveat that keeps this honest is that the analogy holds institutionally, not yet industrially: EVs, solar, and LEO broadband all matured into real commercial closed loops; orbital compute has none yet. The committees and consortia do not prove the technology works. They prove that, regardless of a 2027 horizon, China intends to be organised around it. That is a real and underrated fact — and AI1's June unveil functions inside China not as a rival's spec sheet but as external validation that sharpens the domestic case.

4. The Capital Is Layering — Read the Layers, Not the Headline Numbers

Chinese capital is not flowing into "orbital compute" as one thing. It is flowing into four distinguishable layers, and conflating them is the most common analytical error. Separate them, attach the verified financings, and flag where a number is unconfirmed.

| Layer | Representative example | What it signals | How fundable |

|---|---|---|---|

| 1 — State-backed infrastructure | Orbital Chenguang (轨道辰光): Pre-A1 (Apr 2026) + RMB57.7B strategic credit lines from 12 state banks^[4]^[8] | National intent; de-risks the launch curve | Politically fundable; not a validated business model — credit line ≠ drawn cash |

| 2 — Market-VC component & software | Tiansuan (angel/angel+), Yiwei (seed/angel), Qingbo (angel) — tens-to-hundreds of millions RMB^[4] | Return-seeking bet on subsystem demand from whoever builds constellations | Defensible thesis; modest cheques; component/software exposure |

| 3 — Rocket firms reaching downstream | iSpace (星际荣耀): RMB5.037B D++ (Feb 2026, single-round record); Xingtu Cekong 156-sat SSA constellation; Sugon compute-network^[9]^[10] | Launch firms monetising position by taking stakes in the payload economy | Bankable where tied to launch cash flow, not vertical-stack ambition |

| 4 — Support-layer IPOs | MinoSpace (微纳星空): STAR Market application accepted May 11, 2026, ~RMB5B (~US$736M)^[11]; Emposat (航天驭星) eyeing a listing^[12] | The boring, real businesses — buses, TT&C, ground | Most bankable: funded whether or not orbital AI closes its loop |

Layer 1 — State-backed infrastructure bets. This is the headline-grabbing, policy-driven money. The clearest case is Orbital Chenguang, whose Pre-A1 round in April 2026 was paired with strategic credit-line agreements from twelve state banks totalling RMB57.7 billion — a number our reality check already dissected and which we do not re-prove here.^[4]^[8] The critical caveat bears repeating because Chinese equity markets briefly mispriced it: a strategic credit line is not drawn cash. When listed shareholder Shunho had to issue a clarification and the stock hit limit-up on the RMB57.7B figure, that was the market making exactly the category error this layer invites — reading mobilisation capacity as committed capital.^[8] State-infrastructure money signals national intent and de-risks the launch curve; it does not validate a business model.

Layer 2 — Market-VC component and platform bets. Underneath the state layer, conventional venture capital is funding the picks-and-shovels: spaceborne compute platforms, OS and software, optical components, photonic chips. The reality check captured the representative rounds — Tiansuan's angel/angel+ (Shenzhen Capital Group, SMIC-linked), Yiwei's seed/angel, Qingbo's angel — all tens-to-hundreds of millions of RMB, all component- or software-layer.^[4] The signal is different in kind: return-seeking capital betting on subsystem demand from whoever builds constellations, which is a more defensible thesis than betting on any single constellation closing its economics.

Layer 3 — Upstream-to-downstream extension by rocket companies. The most strategically interesting capital move is launch firms reaching down the stack. iSpace is the cleanest example: in February 2026 it raised RMB5.037 billion in a D++ round — a single-round record for a Chinese commercial-rocket company — while iterating its reusable Hyperbola-3 toward a 2026 first-flight-and-recovery attempt.^[9] iSpace is not building orbital AGI; it is extending downstream pragmatically — its subsidiary Xingtu Cekong (星图测控) announced a 156-satellite "Star Eye" space-situational-awareness constellation from H1 2026, and iSpace partnered with Sugon (中科曙光) to build an open "space compute-network" spanning user, edge, space-cloud, and ground-cloud.^[9]^[10] This is a rocket company monetising its launch position by taking equity and partnership stakes in the payloads it lifts — not by pretending to replicate SpaceX's full vertical stack.

Layer 4 — Support-layer IPOs (the unglamorous, bankable layer). The capital event with the most disclosure is MinoSpace, whose STAR Market IPO application was accepted May 11, 2026, seeking roughly RMB5 billion (~US$736M) to build phase one of its NDRC-approved 112-satellite Taijing constellation.^[11] The prospectus is the clearest financial window in the sector: 2025 revenue of RMB385 million (core aerospace product revenue up ~1,692% year-on-year), a 2025 net loss of ~RMB181 million (narrowed from much heavier prior-year losses), cumulative three-year losses of roughly RMB1.09 billion, and top-five customer concentration of 92.33%.^[4]^[11] Two things matter. First, MinoSpace is a satellite manufacturer, not a compute platform — its "500 TOPS space supercompute" line is marketing-adjacent, and its real exposure to orbital compute is as a bus supplier to constellations including the Qianfan/G60 and Guowang ecosystems. Second, alongside it, TT&C and ground-segment operator Emposat (航天驭星) is positioning for a mainland/Hong Kong listing to fund global ground-station build-out.^[12] These are the boring, real businesses — manufacturing and ground infrastructure — that get funded whether or not orbital AI ever closes its loop. That is precisely why they are bankable.

The layered read yields a sharp conclusion: the further a Chinese player sits from the speculative "compute in orbit" thesis and the closer it sits to a certain industrial input — buses, ground stations, optical modules, TT&C — the more legible and fundable its capital story. The state money chases the vision; the durable money chases the inputs.

5. In-Orbit Reality vs Commercial Closed Loop: The Gap Is Still Enormous

Institutional momentum and layered capital can create an impression of imminence the in-orbit facts do not support. The discipline is the same one the SpaceX teardown applies to AI1: separate verified capability from narrative.

The verified Chinese in-orbit assets remain small. The strongest single case is Zhejiang Lab's Three-Body Computing Constellation — 12 networked satellites launched May 2025, 744 TOPS per satellite, 5 POPS across the network, 100 Gbps inter-satellite laser links, and an 8-billion-parameter model running in orbit, with a long-term target near 1,000 satellites / 1,000 POPS around 2030.^[4]^[13] Three-Body is world-class in system integration and demonstration, not in compute scale — and that distinction is the whole reality check in one sentence. 5 POPS is roughly the throughput of only a few ground-based AI server racks. As a first-in-orbit, integer-precision networked-compute demonstration it is genuinely impressive; as commercial throughput it is negligible against terrestrial clusters running tens of thousands of GPUs. The milestone is the networking and in-orbit operation, not the scale.

The commercial-closed-loop evidence is weaker still, and the reality check's numbers are unforgiving. Guoxing Aerospace, the operator with the most AI satellites in orbit (22) and the reported first general LLM (Qwen3) deployment in orbit, disclosed a 7.62% gross margin on its AI compute satellites — roughly RMB1.4 million of gross profit per satellite, nowhere near enough to fund the R&D, networking, and scaling a commercial constellation requires — across a business that filed for a Hong Kong listing three times.^[4] Orbital Chenguang's in-orbit Chenguang-1 carries compute described by its own project lead as roughly equal to one terrestrial server, against a gigawatt-class vision — a gap of millions of times.^[4] No Chinese orbital-compute operator has yet shown a paying, repeatable commercial workload at scale.

One fresh data point is worth adding, because it cuts both ways. In April 2026, Guoxing and Shanghai Jiao Tong demonstrated remote control of a ground-based humanoid robot via in-orbit compute — a real capability demonstration that hints at latency-tolerant, edge-style use cases.^[7] It is also exactly the kind of demo that proves technical possibility without proving commercial demand: impressive in a press event, unproven as a revenue line. The honest synthesis matches the reality check's: China's orbital-compute sector is in early validation — a small number of real in-orbit facts, a large volume of financing narrative, and no demonstrated commercial closed loop. AI1 does not change that on either side of the Pacific.

6. The Core: What Chinese Builders Should Actually Do

This is the part that matters. If the institutional and capital momentum is real but the commercial closed loop is absent, the operative question for a Chinese founder or incumbent is not "is orbital compute the future" — key state institutions have decided the sector is important enough to organise around — but "given my position, which layer do I play, and what are the honest odds."

6.1 A startup-positioning matrix

Four positions are available; they are not equally good, and most founders should be honest about which is realistically open to them.

| Layer | Risk | Reward | Ceiling | Who it suits |

|---|---|---|---|---|

| (a) Supplier to the national champions — thermal, rad-tolerant payloads, optical-link modules | Low | Stable but capped | Components-margin business; buyer's-market squeeze (cf. Guoxing's 7.62%) | Most teams; especially thermal specialists, given China's documented weakness there^[4] |

| (b) Define the standards & interfaces — the "Android of orbital compute" | Medium | The largest prize on the board | Closed to almost everyone without flight heritage or a state mandate | Only Zhejiang Lab, the CASC system, GEOVIS/Sugon, the CAICT committee^[4]^[2] |

| (c) Find the missing commercial scenario — the repeatable workload that needs orbit | Very high | Winner-take-all | Highest failure rate in the field | Venture-style portfolio bets, not sure things |

| (d) Neutral-export subsystems & services — sellable across multiple compliant ecosystems | Medium, legally bounded | Real, geography-constrained | Capped by export-control / licensing regimes | Operators with cross-border compliance capacity |

On (a): being a supplier in a buyer's market of state programmes can mean Guoxing-style margins. High barrier protects you; concentrated state demand caps you. On (b): a startup that announces a standard nobody is required to adopt has produced a slide, not a moat — standards-setting in practice belongs to whoever already owns in-orbit assets and convening power. On (c): this is the only winner-take-all layer and where most attempts will die — onboard remote-sensing inference, latency-tolerant edge serving where terrestrial power is saturated, sovereign in-region compute are candidates, none yet a proven repeatable revenue line. Layer (d) is covered below, because it is where the China-specific geopolitics bite.

6.2 Why China's cost structure makes "expensive marginal capacity" read differently

The central economic finding of the broader teardown is that orbital compute wins, if at all, as expensive marginal capacity — a relief valve for terrestrial power scarcity, not a cheaper product. For China, two structural facts make the commercial-closed-loop bar even higher than for SpaceX, even as deployment is more politically funded.

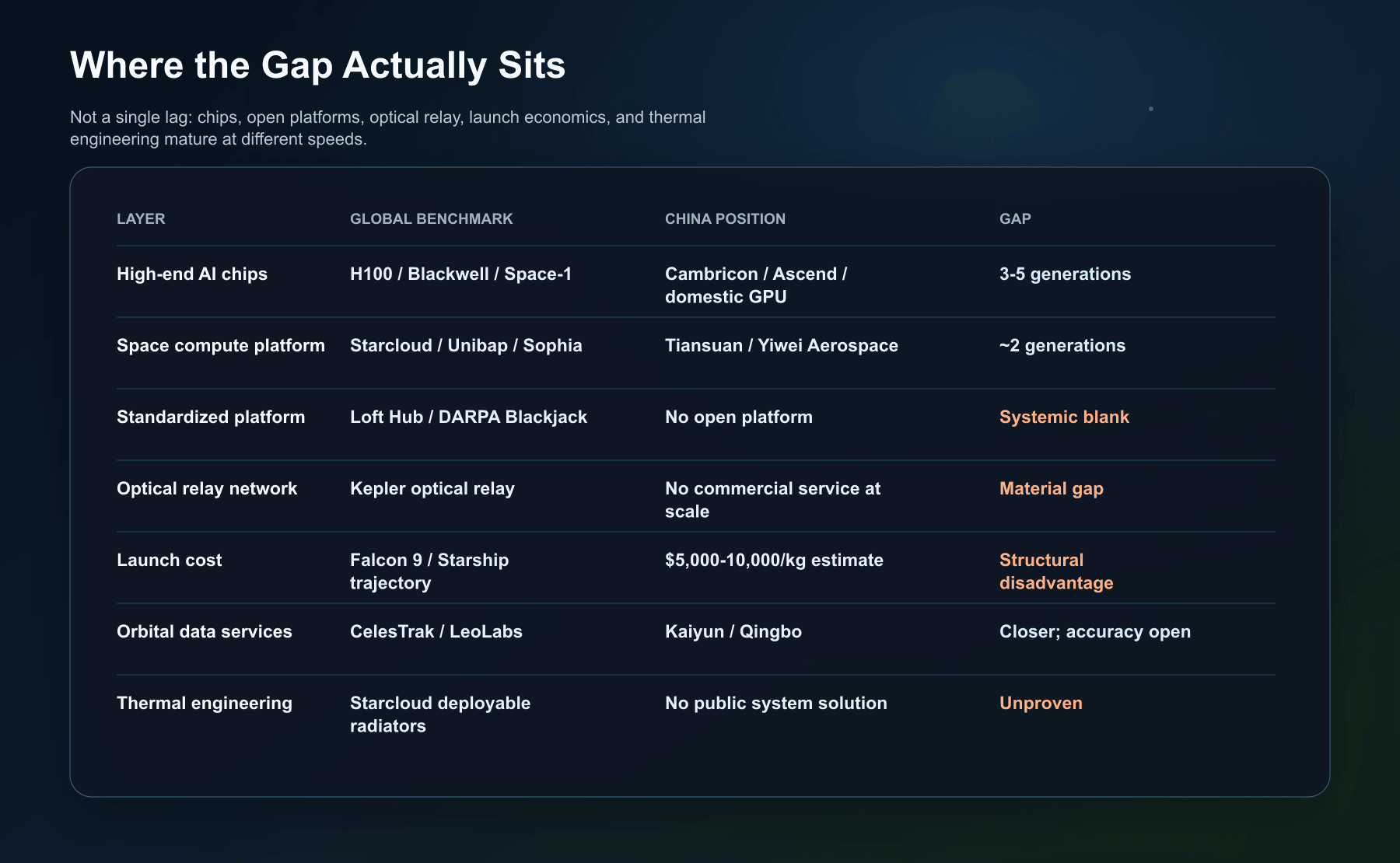

- Launch cost. China has no reusable rocket flying at Falcon-class economics yet. Publicly cited estimates of roughly US$5,000–10,000/kg — not audited marginal costs — sit far above Falcon 9's ~$2,700/kg and an order of magnitude above Starship's $100/kg target, and the whole orbital-compute economic case is a leveraged bet on launch cost.^[4] LandSpace's Zhuque-3 is the variable to watch: its maiden flight on December 3, 2025 reached orbit but the first-stage recovery failed; the company plans a further recovery test in Q2 2026 and a first recovery-and-reflight attempt in Q4 2026.^[14] Until that closes, the gap is real today. The deployment-cadence math is brutal on China's terms: a Zhuque-3 designer stated China would need on the order of 500 medium-to-large launches per year to meet planned satellite deployment — against roughly a dozen commercial launches in 2025.^[7] That is the launch wall in one number.

- The silicon path. SpaceX's answer to radiation is to co-design commercial-node silicon with redundancy. China's situation is narrower than "no access to AI chips": access to the highest-performance US-origin accelerators and the leading-edge manufacturing ecosystem is constrained under export controls. China still has domestic accelerators (Cambricon, Ascend) that lag in peak performance, hardened domestic parts, non-restricted process nodes, and FPGA/ASIC/photonic routes — but each path carries a performance, maturity, or cost penalty.^[4] The constraint is not "no silicon"; it is that the best available path is gated.

Net: China can fund deployment politically further and faster than the market alone would, but the unit economics it must eventually close are harder than SpaceX's — higher launch cost, gated access to the best silicon, policy-driven rather than return-driven capital. Belief is cheaper to mobilise in China; profitability is more expensive to reach. A founder who internalises that asymmetry will choose layers (a) and (d) over (b) and (c) unless they have unusual structural advantages.

6.3 The sovereignty-hedge export model — as analysis, not an evasion playbook

There is a real commercial logic for Chinese LEO operators that has nothing to do with out-engineering SpaceX: serve customers who do not want to depend unilaterally on a US-controlled system. The precedent is visible in connectivity, not compute. Qianfan's operator, Spacesail, has signed an MoU with Malaysia's Measat (February 2025, covering LEO broadband, direct-to-device, and IoT), an agreement with Brazil's state telecom Telebras (services launching 2026), and established a subsidiary in Kazakhstan.^[15] Read the pattern, not any single deal: states and incumbents seeking a non-US, in-region, sovereignty-sensitive option are a genuine market — and as orbital compute matures, the same logic (local data residency, non-dependence on a single foreign provider) extends from bandwidth to compute.

Two hard boundaries, stated plainly. First, this sovereignty-hedge reading is the author's inference, not a stated motive of the operators — their own materials frame these as multi-orbit and connectivity partnerships, and we do not attribute motives the sources do not state. Second — a guardrail, not a footnote — the legitimate version of this play is to compete on sovereignty, non-US-dependence, and local data residency where export-control, security, and licensing regimes permit. It is not to structure entities to evade US rules. This platform does not provide control-evasion guidance, and a Chinese operator's realistic addressable market here is bounded precisely by what those overlapping regimes allow. The opportunity is real; it is also legally constrained, and pretending otherwise is the failure mode.

6.4 The pragmatic play: satellite-borne networking

If there is one near-certain B2B order stream in this entire field, it is not orbital AGI — it is the compute inside every networked constellation. Every one of China's planned tens of thousands of communication satellites (Qianfan's 14,000+, Guowang) needs a spaceborne "brain": routers and switches, space-qualified core-network silicon, inter-satellite routing, real-time control, protocol processing, and orbital orchestration software. Yiwei Aerospace's discipline in choosing exactly this niche — communication-satellite compute, a certainty-demand market that does not require a speculative space-AI boom — is, on the reality check's reading, the clearest strategic logic among the Chinese companies reviewed.^[4] For both startups and incumbents, this is the grounded bet: a constellation must buy this layer to function, regardless of whether orbital data centres ever pencil out. Bet on the network that has to exist, not the AGI that might.

6.5 Lessons for incumbents

The right move depends on which asset you already own.

- Rocket firms (iSpace, LandSpace, CAS Space): extending downstream is correct — but the edge is launch, and it should be traded for equity, data, and partnership, not spent cloning SpaceX's full stack. iSpace's pattern (downstream via Xingtu Cekong, an open compute-network with Sugon) and the 超智算一号 "first-rocket-first-satellite" integration on CAS Space's Lijian-1 — a compute satellite launching H2 2026 as the seed of a planned 1,000-satellite constellation — are the right shape: monetise the launch position by taking stakes in the payload economy.^[9]^[10]^[16] The cautionary note is that the proliferation of "thousand-satellite constellation" announcements is running far ahead of the 500-launches-a-year cadence any of them would require.^[7]^[16]

- In-orbit operators (Zhejiang Lab / Three-Body, Guoxing): the asset to sell is operating experience, not satellite count. The defensible product is "orbital compute as a service" — networked in-orbit operation, the space OS, the in-orbit model, the inter-satellite scheduling — packaged as capability others can buy, rather than a race to launch the most spacecraft into a 7.62%-margin business.^[4] Three-Body's genuine moat is that it has run a networked compute constellation in orbit; that know-how is worth more than the 12 satellites themselves.

- Photonic and optical-compute players (Dongfang Tiansuan, with Photonic-Core / 光本位): the differentiated route — photons are inherently radiation-tolerant and lower-heat, and the path sidesteps the GPU export-control ceiling — is genuinely interesting and globally early, with a reported first space-based photonic-compute payload in joint development in Shanghai.^[4]^[5] But it is years from useful in-orbit AI throughput; treat it as a long-dated option, funded as such.

- Ground-DC and standards players (GEOVIS/Sugon, CAICT-aligned): choose deliberately between a sales-funnel posture (sell ground compute and integration into constellations) and a product-integration posture (own the space-ground compute architecture and its interfaces). The standards prize is real but accrues to those with convening power and flight assets — which these players, uniquely among Chinese commercial entities, partly have.^[4]

7. What's Verified vs Institutional Picture vs Inference

Credibility on a sector this fast-moving and this Chinese-language-sourced depends on being explicit about epistemic status. The table separates three columns: document- or official-verified, the institutional picture built from reporting, and the author's inference.

| Document- / official-verified | Institutional picture (built from reporting) | Author's inference |

|---|---|---|

| SASTIND opened a feasibility study for a space-based intelligent computing constellation (named official, Apr 5)^[1] | Q2 2026 is a coordinated mobilisation (committee + innovation centre + consortia + study read together)^[2]^[3]^[5]^[6]^[7] | China's deployment will be funded ahead of economics it has not closed |

| Space Computing Power Professional Committee formed under CAICT (Apr 3)^[2] | The capital is layering into four distinguishable pools | The picks-and-shovels layers are the ones that survive if the belief is early |

| Three-Body specs: 12 sats, 744 TOPS/sat, 5 POPS, 100 Gbps ISL, 8B model (Zhejiang Lab)^[13] | Orbital compute has no commercial closed loop in China (Guoxing margin, Chenguang single-server) | The "EV/solar/LEO" analogy holds institutionally, not industrially |

| MinoSpace prospectus financials (STAR Market, accepted May 11)^[11] | RMB57.7B "credit line ≠ cash" is a market mispricing, per clarification + limit-up^[8] | The sovereignty-hedge demand reading for Spacesail's deals^[15] |

| Zhuque-3 maiden flight Dec 3 2025, recovery failed; Q2/Q4 2026 plan^[14] | iSpace D++ record and downstream moves (single-aggregator + company site)^[9]^[10] | China's unit economics are harder to close than SpaceX's |

The excluded items are as important as the included. Two reviewer leads — a Suzhou "compute-satellite" Pre-A and an iSpace compute-subsidiary name — could not be independently sourced and are excluded entirely. The silicon-constraint claim is narrowed to the highest-performance US-origin accelerators and leading-edge manufacturing, not to "AI chips" broadly.

8. What It Means for Asia-Pacific / Singapore

For Singapore and the wider APAC neutral nodes, the realistic posture is narrow and worth stating without inflation. The instinct to "serve both sides" of a US-China orbital-compute split is legally constrained, not free: export-control, security, and licensing regimes mean the achievable position is "serve multiple compliant ecosystems where the regimes permit," not a frictionless bridge between blocs.

Within that boundary, Singapore's assets are specific and real, not aspirational: optical ground stations and a neutral data-landing point that constellations of either origin can use where compliance allows; a photonics and precision-engineering base that maps onto optical-link and thermal subsystems — the same layer (a) Chinese suppliers will compete in; and a credible role as a standards-convening venue for payload interfaces and cross-border compute-data governance, the rule-setting layer that, unlike launch or silicon, does not require capital Singapore cannot match. None of this is fielding an AI1. All of it is sellable. The frame to reject is "build our own orbital compute"; the frame to adopt is "land the data, set the rules, and supply the components — for whichever compliant ecosystems will buy." This coda is deliberately modest: Singapore has no launch vehicle, no in-orbit compute asset, and no state programme pointed at this, and pretending otherwise would be the inflation this platform exists to avoid.

9. What to Watch

Five China-specific, dated signals would confirm or break the thesis.

- Zhuque-3 recovery and launch cadence (Q2–Q4 2026). Watch whether LandSpace's Q2 recovery test succeeds and the Q4 recovery-and-reflight attempt closes — and whether anyone begins to approach the ~500-launches-a-year wall.^[14]^[7] Reusability at Falcon-class economics is the single fact that would most change the China unit-economics call.

- The first commercial closed loop. The thesis breaks the day a Chinese operator shows a paying, repeatable workload at scale — not a press-event demo. Until then, the in-orbit-vs-narrative gap stands.

- MinoSpace IPO outcome and disclosures. Whether the STAR Market listing completes, at what valuation, and what further the prospectus and any follow-on filings reveal about real demand versus customer concentration.^[11]

- A photonic-compute payload reaching flight. The first space-based photonic-compute payload actually flying (vs in joint development) would validate the one route that sidesteps the silicon ceiling.^[5]

- Feasibility study → funded programme. Whether the SASTIND study and the CAICT committee produce an actual funded national programme and deployment plan, or stop at a feasibility study and an industrial committee. The distinction — feasibility study vs industrial committee vs official national programme vs funded deployment plan — is the difference between mobilisation and intent.^[1]^[2]

China-specific data here is drawn from public sources including: Xinhua and China News Service reporting on the April 2026 Space Computing Industry Conference; SASTIND and CAICT statements; the Pujiang Innovation Forum and CCF YEF2026 materials; STAR Market and HKEX prospectus disclosures (MinoSpace, Guoxing) and SpaceNews/SatNews coverage of them; Sina Finance, 36Kr, and People's Daily reporting on company financings and the 超智算一号 and Three-Body programmes; and this platform's own prior verified work on China's orbital compute sector. Several figures originate in Chinese-language reporting and are flagged in-line and in the source grades where they are not independently corroborated; two reviewer leads (a Suzhou compute-satellite Pre-A and an iSpace compute subsidiary) could not be sourced and were excluded. The sovereignty-hedge reading of Chinese LEO export deals is the author's analytical inference, not a stated motive of the operators. Analysis represents the author's independent views and is not investment advice. Nothing here is an endorsement of any company.

Sources

- 1.Xinhua (english.news.cn) — China starts feasibility study for space-based intelligent computing constellation(english.news.cn)

- 2.China News Service (中新网) — 业界首个太空算力产业协同平台"太空算力专业委员会"成立(chinanews.com.cn)

- 3.Xinhua / NCSTI & Beijing Daily (北京经开区) — 2026太空算力产业大会在北京经开区举办:太空算力专业委员会成立、北京太空算力创新中心启动(ncsti.gov.cn)

- 4.Singapore Space Agency — China's Orbital Compute Reality Check

- 5.The Paper (澎湃新闻) — 长三角天基计算创新联合体成立,抢抓弯道超车机遇(m.thepaper.cn)

- 6.China Computer Federation (CCF) — YEF2026 | 太空算力:如何突破概念验证迈向规模部署?(ccf.org.cn)

- 7.Xinhua (新华网) — 市场最前沿丨将算力"搬"上天,我国加快太空算力产业生态培育(news.cn)

- 8.Sina Finance (新浪财经) — 577亿元!轨道辰光完成Pre-A1轮股权、债权融资 / 太空算力大牛股紧急澄清(finance.sina.com.cn)

- 9.Future Phecda (未来天玑) — 2026中国10大商业火箭公司 / iSpace D++ round and downstream moves(futurephecda.com)

- 10.Zhihu industry compilation (慧博出品 via 知乎) — 太空算力深度:需求分析、商业部署、产业链及相关公司深度梳理(zhuanlan.zhihu.com)

- 11.SpaceNews — Chinese satellite maker MinoSpace seeks $736 million in IPO(spacenews.com)

- 12.SatNews — Space Race Moves to Wall Street: China's Private Rocket Makers Target IPOs as Historic SpaceX Flotation Nears(satnews.com)

- 13.Sina Finance (新浪财经) — 之江实验室:我国整轨互联太空计算星座"三体计算星座"进入组网阶段(finance.sina.com.cn)

- 14.Xinhua (english.news.cn) — China's LandSpace plans new recovery test for Zhuque-3 reusable rocket in 2026(english.news.cn)

- 15.SpaceNews — Chinese constellation operator Spacesail signs agreement with Measat of Malaysia(spacenews.com)

- 16.People's Daily / Sina Finance (人民网/新浪财经) — "超智算一号"算力卫星在京首发(finance.people.com.cn)

Continue reading

22 Jun 2026 · 42 min read

AI1 and SpaceX's $1.77 Trillion IPO: What the Orbital-Compute Option Is Actually Worth

AI1 is a credible engineering option, not a proven business: the gap between Musk's unveiling and SpaceX's own S-1 risk language is the investment case.

12 Jul 2026 · 98 min read

The Third Pole in Orbit: OneWeb's Soul, DayOne's Method

A Singapore-founded Indo-Pacific orbital-compute venture is buildable only as a phased, demand-anchored operating company whose multi-sovereign capital cannot control it.

28 Apr 2026 · 45 min read

The Orbital Compute Contest: US-China Space Data Centers and Three Windows for Asia-Pacific

From Meta's space-based power deal and SpaceX's million-satellite orbital data center filing to China's state-capital response through Orbital Chenguang, this article examines how orbital compute could reshape AI infrastructure and where Asia-Pacific can realistically win: validation infrastructure, standardized subsystems, and rule-setting.